Auto Loans

Feeling stuck under the weight of car loan payments? You’re not alone, and it’s never too late to turn things around. Whether it’s refinancing, accelerating payments, or exploring smarter financial strategies, you can reduce the burden and regain control. With the right plan and guidance, you’ll be on the road to financial freedom sooner than you think.

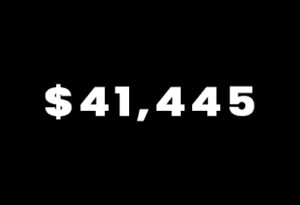

Average New Car Loan

In Q4 2022, the average amount financed for new car loans was $41,445, a 17% increase since Q4 2020.

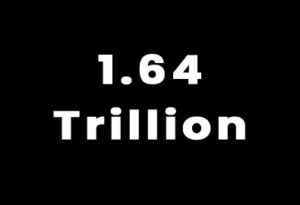

Record Auto Loan Debt

As of Q3 2024, Americans owe approximately $1.64 trillion in auto loan debt, marking a 3.1% year-over-year increase.

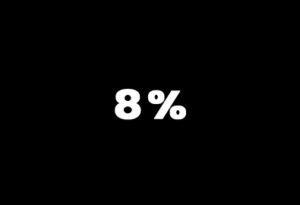

Late Payment Rate

Approximately 8% of auto loan balances transitioned into delinquency over the past year, with subprime and near-prime delinquency rates now at or exceeding levels observed during the Great Recession.

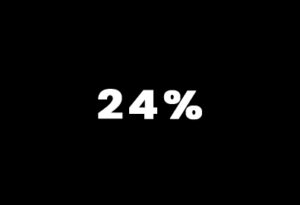

Negative Equity

Approximately 24% of vehicles traded in the recent quarter had negative equity, meaning owners owed more on their loans than the cars’ worth.

Coaching and Tools

The Weight of Auto Loan Debt

Auto loans can quickly become a burden, especially with rising interest rates and extended loan terms. Many borrowers face high monthly payments or owe more than their car’s value, making it hard to stay ahead financially. Understanding your options and taking proactive steps can help lighten the load and put you back in the driver’s seat!

Strategies for Financial Freedom

Whether it’s refinancing your loan, negotiating better terms, or accelerating payments, there are ways to manage auto loan debt effectively. With the right guidance, you can reduce your debt, free up your budget, and move toward financial stability—all while staying on the road.

Tools to Use On Auto Debt

Refinance for a Lower Interest Rate

- How it Helps: Refinancing can reduce your monthly payment or overall interest costs, especially if your credit score has improved since you took out the loan.

- Action Step: Shop around for refinancing options through banks, credit unions, or online lenders. Use a loan calculator to compare potential savings.

- Pro Tip: Ensure refinancing doesn’t extend your loan term excessively, as that could increase the total amount paid.

Make Extra Payments Toward the Principal

- How it Helps: Paying more than the minimum reduces the loan balance faster, cutting down on the interest you’ll owe.

- Action Step: Round up your monthly payment or make a lump-sum payment whenever possible. Verify with your lender that extra payments are applied to the principal.

- Pro Tip: Schedule extra payments right after your regular ones to maximize the impact on principal reduction.

Avoid Negative Equity (Being Upside-Down)

- How it Helps: Negative equity occurs when your car’s value is less than the loan balance, making it harder to sell or trade in the vehicle.

- Action Step: Minimize this risk by avoiding long-term loans (over 60 months) and putting down at least 10-20% upfront when purchasing a car.

- Pro Tip: If you’re already upside-down, focus on aggressive payments to reduce the loan balance faster and avoid rolling negative equity into a new loan.