Mortgages

A mortgage can be one of the biggest financial commitments you’ll ever make, but it doesn’t have to feel overwhelming. Whether you’re looking to pay off your home faster, refinance for better terms, or manage your payments more effectively, there are strategies to help you stay in control. With the right guidance, you can navigate the complexities of home financing and work toward a future of financial freedom and stability.

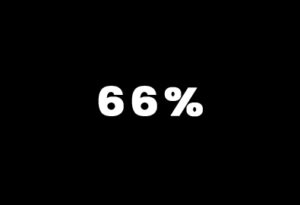

Percent of Americans who own their home

As of the third quarter of 2024, the homeownership rate in the United States was 65.6%, indicating that approximately two-thirds of American households own their homes.

Record Mortgage Debt

Americans owe $12.59 trillion on 84.94 million mortgages, averaging $148,222 per person with a mortgage on their credit report.

Poor Credit Penalty

As of early 2025, borrowers with FICO scores between 760 and 850 secured an average annual percentage rate (APR) of 7.242% on a 30-year fixed-rate mortgage. In contrast, those with scores between 620 and 639 faced an average APR of 7.838%. This difference can lead to an additional $36,700 in finance charges over the life of the loan.

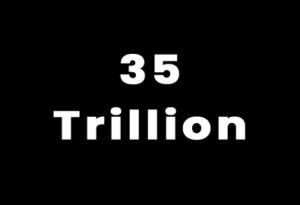

Total Home Equity

U.S. homeowners collectively hold a record $35 trillion in home equity, more than double the amount before the 2008 housing crash, reflecting significant increases in home values.

Coaching and Tools

The Importance of Credit Health

Maintaining a strong credit score is one of the most effective ways to reduce the cost of homeownership. Higher scores not only make you eligible for lower interest rates but also free up your budget for other financial priorities. If your score needs improvement, taking steps like paying down existing debt, avoiding new credit inquiries, and addressing any inaccuracies on your credit report can make a significant difference. The financial benefits of better credit extend far beyond monthly savings, helping you build long-term stability and wealth.

The Path to Better Mortgage Rates

Improving your credit score before securing a mortgage can save you thousands of dollars and provide more financial flexibility. Start by checking your credit report for errors, paying down existing balances, and maintaining a low credit utilization ratio. Small changes can lead to significant improvements over time, opening the door to better loan terms. By being proactive, you can reduce your borrowing costs and make homeownership a more affordable and rewarding investment.

Tools to Use On Mortgage Debt

Make Extra Principal Payments

- How it Helps: Extra payments toward the principal reduce the loan balance faster, saving you money on interest.

- Action Step: Add an extra amount to your monthly payment (e.g., $100) or make a lump sum payment whenever possible.

- Pro Tip: Check with your lender to ensure extra payments are applied to the principal, not future interest.

Negotiate a Lower Interest Rate

- How it Helps: Refinancing can reduce your monthly payments and total interest costs over the life of the loan.

- Action Step: Shop around for lenders offering lower rates and calculate the breakeven point (how long it takes savings to cover closing costs).

- Pro Tip: Consider refinancing into a shorter term (e.g., 15 years) if you can afford slightly higher payments—it significantly reduces interest paid overall.

Explore Loan Modification or Forbearance Options

- How it Helps: If you’re struggling financially, these options can temporarily reduce payments or pause them entirely.

- Action Step: Contact your lender to inquire about loan modification programs or forbearance policies. Be prepared to provide proof of hardship.

- Pro Tip: Keep communication open with your lender—early action can prevent foreclosure and help you negotiate better terms.